This is a stock that caught my eye 3 years ago as a value play, and I took a long position. But as I continued to research this company I kept running into red flags. .. questionable accounting, insider transactions, and a CFO that had presided LIWA -- which was delisted for accounting fraud. Not exactly the type of management I want running companies I have my money in, so I sold for a small loss. It was a good thing I did, shortly after I bailed, the company's stock price took a huge hit after it announced that it had to re-state and several seeking alpha articles, which discussed the insider dealings.

Here is my thesis for a short position

PME has been running and has been promoting itself on a a weekly TV finance program in China --- i.e. PAID promotion. That is always a red flag:

Here is my thesis for a short position

PME has been running and has been promoting itself on a a weekly TV finance program in China --- i.e. PAID promotion. That is always a red flag:

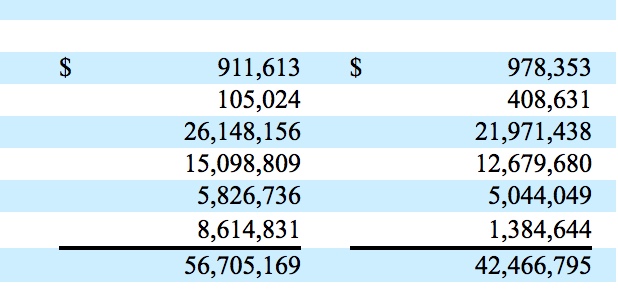

Worse, Financial Weakness:

The last 10Q shows that revenue has fallen off the cliff and losses are quickly increasing.

CASH -

Only 12 Mill down in cash position

Current liabilities:

56.7 Million!

Also debt has been growing over recent quarters. They are down to their last 500K and they are paying a dividend? Does that make sense? It does once you realize that the largest shareholders are the insiders.

PRIOR FINANCIAL IMPROPRIETIES

The biggest concern for this company is that the insiders have treated it as their personal piggy bank. A couple of years Ago there was a Seeking Alpha Article that that detailed all "Fishy Business" going on at PME.

"Chinese fishing group Pingtan Marine Enterprise has announced a restatement of its finances for the years 2012 and 2013, which resulted in shaving $187 million off its stockholder equity.

The change also reduced total assets by $188m."

LINK Essentially, what PME was doing was it was counting ships it had leased from INSIDERS as its own.

The Insiders have continued to treat this PME as their personal piggy bank.

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS

The 10Q reflects numerous related party entries. I have never seen a company with more insider dealing.

The quarterly report reflects that all aspects of the supply chain are being paid to businesses owned by insiders.

The vessels

"On June 26, 2015, we entered into a master agreement with each of Fuzhou Honglong Ocean Fishery Co., Ltd, (“Hong Long”) and Fuzhou Yishun Deep-Sea Fishing Co., Ltd. (“Yishun”), which are owned by our Chairman and CEO, Mr. Xinrong Zhuo, for the acquisition of 6 fishing vessels with total consideration of approximately $56.2 million representing the fair market value on the date of acquisition."

Office Space

Office Space

On July 31, 2012, Pingtan Fishing entered into a lease for office space with Ping Lin, spouse of the Company’s CEO, (the “Office Lease”).

On July 1, 2013, we entered into a service agreement with Hai Yi Shipping Limited that provided us a portion of use of premises located in Hong Kong as office and provided related administrative service (the “Service Agreement”). ... For the year ended December 31, 2015, rent expense and corresponding administrative service charge related to the Service Agreement amounted to $462,387.

SERVICES (FUEL and Maintenance)

During the year ended December 31, 2015, we made purchase of fuel, fishing nets and other on-board consumables from PT. Avona Mina Lestari, Hong Fa Shipping Limited, Haifeng Dafu Enterprice Co., Ltd., Hai Yi Shipping Ltd., and PT. Dwikarya Reksa Abadi, of approximately $1,276,000, $11,329,000, $11,000, $4,739,000 and $1,415,000, respectively.

During the year ended December 31, 2015, we made purchase of vessel maintenance service from PT. Avona Mina Lestari and from PT. Dwikarya Reksa Abadi of approximately $6,529,000 and $3,207,000, respectively.

During the year ended December 31, 2015, we made purchase of transportation service from Fuzhou Honglong Ocean Fishery Co., Ltd. and from Hai Yi Shipping Limited of approximately $178,000 and $306,000, respectively.

RISKS To Short Position.

Squeeze? Not likely as there are 80 Million shares out standing.

Sudden news? Perhaps if indonesia opens The Company announced that its next earnings would be in March so there shouldn't be any earning surprise news to boost the stock.

Dilution? At the end of December, PME registered a 100 Million Shelf:

Dilution? At the end of December, PME registered a 100 Million Shelf:

CHARTS

From a chart perspective there is a bullish case to be made. Nice rip over the last couple of weeks but running into some supply?

DAILY -- is honoring the resistance levels on the weekly. Volume has been strong on the initial push but it is falling off on Friday's move. RSI is overbought on daily.

CONCLUSION

This is a company that has a sordid history and it appears continue operating at the status quo. The financials are quickly deteriorating and the company is nearly out of cash.

It now appears the company is trying to pump its stock price with paid promotion while at the same time it is preparing to dump a massive amount of shares on the market through its 100 Million Shelf registration.

At the end of the day, this is a fishing company, and this company is more of a fish story than a worth while investment.

Target $1.00

No comments:

Post a Comment